October 1 is on the horizon and that means the FAFSA will be available for students to complete and file. Believe it or not, many students don’t bother completing it and that’s a decision you and your student might regret.

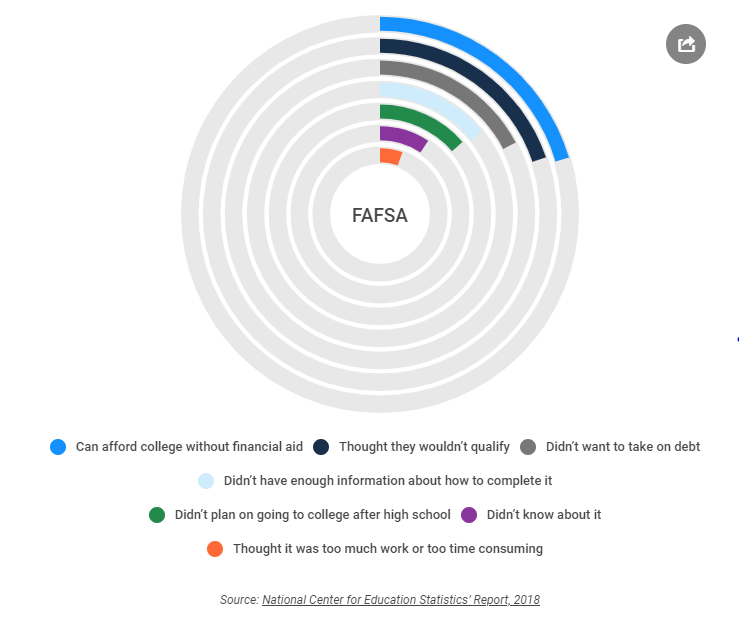

According to the National Center for Education Statistics, Only 65% of high school seniors complete the FAFSA, Why don’t more fill it out? Most either can afford college without financial aid or think they won’t qualify for financial aid. Other reasons include a lack of information — and just planning on skipping college entirely.

Completing the FAFSA is an essential step of the college application.

Why bother completing the FAFSA if you don’t need financial aid?

Even if you and your student can afford to pay for college, why would you pass up free money? Colleges use the FAFSA when distributing merit aid and even some private scholarships require a completed FAFSA.

If you need financial aid, how can completing the FAFSA help?

If you need some form of financial aid to pay for a college education, you MUST complete the FAFSA. In order for students to qualify for federal student loans, state loans, and work-study, they must submit the form. The FAFSA is also required if you plan to take out a Parent PLUS loan to help your student pay for college.

In addition, many students are eligible for federal Pell Grants. High school graduates who didn’t complete a federal financial aid application missed their opportunity for part of $2.6 billion in free money for college, according to NerdWallet’s annual analysis of federal financial aid data.

The money went unclaimed by 661,000 members of the Class of 2018 who were eligible for a federal Pell Grant but didn’t complete the Free Application for Federal Student Aid, or FAFSA.

How much time does it take to complete the FAFSA?

The FAFSA has over 100 questions, which can take anywhere from a half hour to an hour to complete. According to data compiled by Finder.com, new applications less than an hour, averaging 35 minutes. Renewing your application takes even less time — 23 minutes on average. Filling out the FAFSA for the first time takes the longest since you need to fill in answers for each required question.

The bottom line: complete the FAFSA. It doesn’t take that long and most students qualify for some form of financial aid. That doesn’t mean you have to accept it, but why not have that option? And you certainly don’t want to miss out on some of that FREE money!

I

received an email from a concerned parent whose student was going to be

attending orientation next week. In the email, he confessed that he might need

some help with information regarding financing his son’s college education. I was

surprised that he waited so long. Unfortunately, I had to advise him that at

this point his only options were private loans and advise his student to apply

for scholarships over the summer.

Parents should consider college funding even before their student applies to college. The inevitable result of lack of planning is parents and students borrowing to pay and usually borrowing more than they can repay after graduation.

What

do the statistics say?

With

school starting shortly, student loan borrowing often appears in the news. It’s

especially prevalent now with presidential candidates promising to erase

student loan debt. Wherever you stand in the political landscape, it’s clear

from the statistics that students have borrowed more than they can repay.

According

to a 2018 report by the Federal Reserve Bank of New York, as many as 44.7

million Americans have student loan debt, that’s one in five adult

Americans. The total amount of student loan debt is $1.47 trillion as

of the end of 2018 — more than credit cards or auto loans.

How

do you make wise financial choices?

Before applying to college, you and your student should investigate the cost. You can gather the information either on the college website or by using College Navigator. When viewing these figures, you should also research the college’s financial aid statistics—what percentage of students are awarded aid, how much aid is awarded and how much do students typically borrow. Since every family’s financial situation is different, these figures should help determine if the college is affordable to attend.

How

does financial aid play into the equation?

If

you complete the FAFSA, your student will receive some form of financial aid.

The most common is student loans, but colleges also award grants and merit aid

as well. Always complete the FAFSA, even if you don’t think you will qualify

for aid. Colleges use the information on the FAFSA when awarding scholarships

and grants. No FAFSA, no aid.

What’s the key to avoid borrowing too much?

Use repayment calculators before you sign on the dotted line. The rule of thumb is that students should only borrow as much to pay for college as their first year’s salary. By keeping your debt under one year’s salary, you won’t have to put more than about 10% of your income towards student loan payments. Borrowing more than your student can afford to repay sets them up for overwhelming debt after graduation. Your student can look at salary comparisons for their anticipated career at PayScale.com.

How

can you avoid borrowing to pay for college?

The key to not borrowing to pay for college is to receive merit aid, grants, and outside scholarships. Your student should apply to a college at the top of his or her applicant pool. This means the college will be more likely to award aid to attract your student. Grades and standardized test scores are also a key factor in awarding aid. Your student should focus throughout college to pursue excellence in these areas. And, don’t forget outside scholarships. Your student should focus time and effort in applying to every scholarship he or she qualifies for. This means starting early and planning to submit the best application. Click here for scholarship application tips and see how your student can win enough money to pay for college.

Finally, borrow wisely. Only borrow what you need. Your student can borrow the maximum amount, but only borrow what is necessary. Just because you can, doesn’t mean you should. Choose the loans with the lowest interest rates first.

Keep these questions in mind as you plan your next college visits and

take the time to schedule an appointment with the school’s office of financial

aid.

1. What are your

financial aid deadlines?

In addition to deadlines for the standard financial aid applications: the

Free Application

for Federal Financial Aid (FAFSA) and PROFILE, the financial aid application

service of the College Board, colleges may also have their own deadlines and

forms. Be sure to ask if the school’s financial aid forms are different for

need-based and merit-based aid when the deadlines are. Note many schools have

declared March 1 as their priority filing date for financial aid. Be sure to

confirm each school’s priority filing dates.

2. What is your Cost of Attendance (COA) for the current year?

There are precisely six components to a college student’s complete

budget:

Tuition

Fees

Room and Board

College Textbooks and Supplies

Personal expenses

Transportation

Many proposed budgets only include Direct Costs (which are the first three items listed) and typically what you will pay directly to the bursar’s office. However, the U. S. Department of Education requires that colleges fully inform you as to all of the above costs, so find out specifically what those amounts are to establish a complete budget for college expenses.

3. How much of an increase in the COA do you project for next year?

When you ask this question, be sure to request the specifics related to

each cost component. Tuition and Room and Board increases are independent of

each other. For example, one school may expect an increase of 5 percent in

tuition and fees, but a 10 percent increase in Room and Board. This information

will help with budgeting but also gives the financial aid officer the

impression that you are an informed parent.

4. Are you able to meet 100 percent of financial need?

If they say “No,” find out why, and get details. Is the policy

based on “first come, first served?” What’s the average percentage of

need the school can meet? What percentage is in the form of grants and how much

is in the form of loans? Is there a dollar amount left

as a gap (unmet need) for everyone? Do they include Parent Loans (PLUS) in the aid package?

(Note: They shouldn’t do this…those loans are to be used for your EFC-Expected Family Contribution, not for meeting

the financial need of the student.)

5. Do you offer Merit Scholarships, and how do you treat private scholarships awarded to the student?

If a Merit Scholarship is being awarded, it normally goes into the

financial aid package first, reducing the amount of need-based aid. Find out if

a merit award reduces the self-help in the package, or if it replaces other

need-based grants. A true Merit Scholarship can go beyond the “need”

level, which means that it can lower your EFC.

It’s a jungle out there–cluttered with all kinds of college advice. How does a parent hack through the massive amounts of advice and find what they need with confidence? It’s not easy. There are hundreds, if not thousands, of college help websites, Facebook groups, YouTube channels and more offering paid and unpaid advice about college.

There are five experts I turn to when I need added advice about all things college:

Debbie Schwartz-admissions/financial aid

Debbie Schwartz founded Road2College in 2016 to educate families about college admissions and empower smarter college financial decisions. Her facebook group has a huge following with parents and experts sharing advice about paying for college and finding colleges with the best merit aid.

With all the scholarship search sites and information out there, you need someone to help your student WIN the scholarships they are eligible for. Monica fits that bill. She successfully helped her son graduate debt-free with $100,000 worth of scholarships by using her unique method of packaging the scholarship application. She knows her stuff and she knows what you need to know to make the scholarship application process successful.

Perhaps the most complicated aspect of the college application process is financial aid. Jodi has experience in this area from working in a college’s financial aid department. She has advice related to the FAFSA, student loans, financing college and helping your student budget for college. If you have a financial aid question, Jodi knows the answer.

I love Ethan’s information because he knows what he is talking about and much of it is free to anyone who takes the time to browse his website. He offers samples of essays, tips for writing them, brainstorming ideas and more. He also provides personalized help with the essay and web training for students as well. You can’t go wrong by using Ethan’s expertise and he even has a “pay what you can afford” option for his seminars. What could be better?

If you have a learning disabled student or simply a student who can’t seem to focus on preparing for standardized tests, Jenn is the expert. Her unique method of coaching not only helps prepare your student for the test, but she helps them learn study habits to help with more than test prep. Jenn has the training and the experience to help your student do their best on any of the standardized tests. Plus, she’s a Duke alumini and proud of it!

Disclaimer: I don’t receive any fee or commission for recommending these experts. These are simply my own “go to” experts when I have a question or need to collaborate in any of these areas of college prep. I trust them implicitly and you can too!

As the costs of college keep rising each year, many students and their families find it necessary to rely on financial aid to help pay for college. There are many different types of financial aid available, and knowing which one best matches your situation is key to not only choosing the right type of aid, but also maximizing the amount that you can qualify for—and minimizing your debt obligations later on.

Financial aid is a critical part of the college application and attendance process. It can make college a reality for many students and help bridge the gap between family contributions and the overall cost of attendance. Some types of aid don’t need to be paid back; others can leave you in debt for years to come.

With that in mind, it’s important to understand how to best approach the financial aid process, and how to set yourself up for financial success later by putting thought into the process now.

What Should You Start With?

The first step in the financial aid process should be completing the FAFSA. Short for the Free Application for Federal Student Aid, the FAFSA walks you through a complete picture of your finances. If you’re a dependent student—most first-year students are—then it also includes questions about your parents’ financial situation and their potential ability to assist in funding your education.

The federal government is the biggest source of financial aid for college students, and before it’ll consider you as eligible for aid, you’ll need to complete the FAFSA, which serves as your application for all federal aid. The FAFSA is completed online, it’s free, and there is plenty of help available to assist you and your family in filling it out.

What’s the Takeaway from the FAFSA?

Once your FAFSA is submitted to the federal government along with your choices of colleges, a Student Aid Report, or SAR, is generated from the information you entered. The SAR explains how much your expected family contribution (EFC) is. The government takes the position that it’s your responsibility to pay as much as you can to your own education first; the EFC is how much the Department of Education thinks you and your family should be able to contribute to the total cost.

Each year, colleges publish an amount called the cost of attendance. It includes all the expenses that go into attending that school: tuition, room and board, textbooks, fees, and other things like living expenses throughout the school year. Your EFC is subtracted from the Cost of Attendance, and the resulting balance is considered your financial need. The federal government sends your SAR to the schools you listed, and they compile a financial aid package to offer you.

Your federal financial aid package could include a variety of aid products including Pell grants, unsubsidized and subsidized federal student loans, and more. You should always consider Pell grants and subsidized federal aid first. A Pell Grant is a type of aid that does not require repayment, and subsidized loans do not accrue interest while you’re attending school.

After looking at your offer, you may find that your financial aid package isn’t enough to cover the entire bill, but there are other options to consider such as scholarships.

Should You Consider Scholarships?

The short answer is “YES, absolutely!” Scholarships, like grants, are essentially free money that you don’t have to pay back. They should always be a consideration regardless of what year you are in college. You can apply for new ones every year, and there are tons of sources to find scholarships. They can really make up the difference up between the cost of attendance and your financial aid package. Start early and often. If the FAFSA wasn’t so important, this would be the first place to start.

There are thousands of scholarships available every year, but they’re highly competitive. Each program has its own application criteria and deadlines, and the best way to maximize your chances of winning one is to ensure that you follow the program’s directions and meet all of the deadlines—preferably applying as early as possible. The best way to go about winning scholarships is to just keep on applying to any legitimate opportunity you can find.

Is There a Last Resort?

If you find there’s a funding gap left over after scholarships, grants, and other federal aid, then you still have one option: a private student loan. There are distinct differences compared to federal student loans do, but sometimes they’re a necessary tool to cover that funding gap.

Offered by banks, credit unions, and other lenders, private student loans are based upon your creditworthiness; as a result, most students find that they need a qualified cosigner for approval. Further, you may find even the best private student loans still have high interest rates compared to federal loans. After all, interest rates are generally higher for private loans. Also, they don’t come with a grace period like a federal loan. That means you’ll need to start paying it back immediately, just like a car loan or mortgage, even if you’re still in school.

It is clear that private student loans are not as desirable compared to their federal counterparts; however, sometimes they’re a viable option if it’s crunch time.

If receiving financial aid is the key to attending college, you might want to look at your college’s financial aid footprint. Every college reports the statistics related to their financial aid profile. These statistics can tell you how generous they are with their scholarships and grants and also the percentage of students who receive help with their tuition. It will also help you determine if you should ask for more merit aid when you receive your financial aid package. If a college is not generous with aid and your student receives some, it’s unlikely they will award more.

The best resource available for these statistics is College Navigator. You can enter the name of the college, or search using criteria such as location, size, and degree plans. Once you’ve pulled up the data, you can use it to compare colleges.

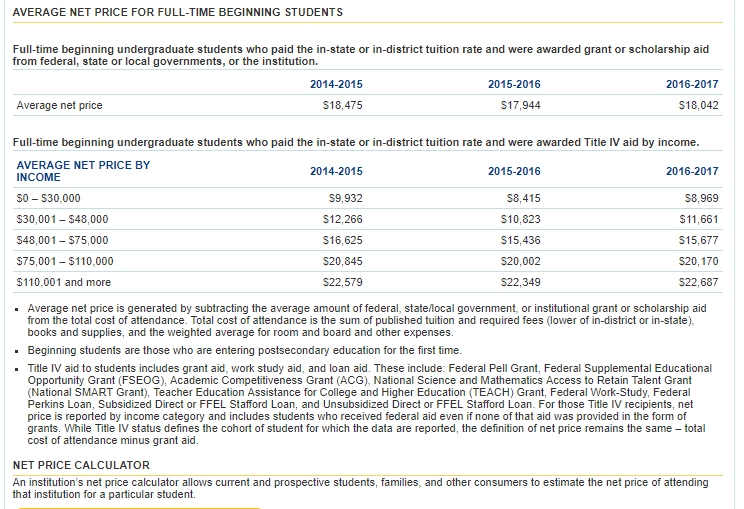

Below is a screenshot of just one university, Ohio State:

As you can see, 67% of the full-time beginning undergraduate students receive aid in the form of grants or scholarships; 70% of that aid is from institution grants and scholarships. Also notable, the average amount of aid received in the form of grants or scholarships per student is $9,275. Total tuition/room and board is $27,037 for in-state, on campus students. Therefore, 1/3 of tuition, room and board is covered in the form of grants and scholarships.

covered in the form of grants or scholarships.

Another valuable part of the information available includes the average net price broken down by household income:

All of this information will help you determine a college’s financial aid footprint and give you the much-needed data you will need to make the wisest financial choice. Finding the college with the best financial aid is part of finding that perfect fit college.

In addition, you can connect with the College Affordability and Transparency Center provided by the federal government to determine which colleges are the highest and lowest priced and which offer the best value.

While many students are busy packing their bags and getting ready to leave for their first year at college, still others are working on their applications for the next round of admissions. Of course, if your child fits the latter category, it’s likely that they already have a college in mind that they wish to attend. Happily, by reading the post below you can find out about the tactics that will help them get into their first choice. Keep reading to discover more.

Address any study or subject issues

Number one of the list tactics is dealing with grades, as this is the base level that a college application will address. Happily, this is something that you can definitely help your child with, without micromanaging them as well. Firstly, it’s vital that you take a keen interest in their progress with their studies, without being overbearing and demanding.

Then, if they or their teachers flag up an issue on a particular topic, it will be much easier to address this constructively. It may be that your child is struggling with a specific subject, or that something is going on in their life that creating a distraction for them. However, as long as you are able to have an honest two-way conversation, you will ultimately be able to get them the support or help they need to ensure that their grades remain on target to get into the college of their choice.

Help your child to present a rounded application

Please do remember though that while grades are essential for college, they are not the only thing that the application board with be looking at. In fact, lately, there has been a definite move towards reviewing the whole person and looking at their extracurricular activities as well as their academic ones.

What this means is that you can quickly help your child by encouraging them to engage in activities outside of the home. These may include sports such as basketball, football, and athletics, as well as getting them involved in community projects like food banks, reading programs, and soup kitchens. Even having a part-time job, or getting some work experience in a firm that is related to their studies can go a long way to helping them stand out amounts all the other candidates. Something that can help them secure that much-needed place in their first choice school.

Seek additional help

It’s also wise to remember as a parent that there is plenty of help out there both for you and your child when it comes to making a successful college application. First off there is lots of advice online that can take you through the process step by step, and also help you hone your child’s particular application documents.

Although, if your child is aiming at one of the top schools in the country it can be helpful to approach specialists like Ivy Select admission consulting for some additional help. After all, as they have been through the process of being accepted to an ivy league college, they are the best people to know all the little tips and tweaks to make to your child’s application for the best chance of them getting into their first choice.

Explore financial aid and scholarship options

Lastly, it is important to remember that it may be finance and scholarship issues that are standing in the way of your child getting into their first choice college. In fact, as university fees have risen so sharply in recent times, it is widespread for students to pick the more economically viable options, rather than where they genuinely want to go.

Luckily you can assist your child in dealing with this, by going through the costs of their course with them, and showing them what sort of budget they will be working on. You can even help them by demonstrating how this will affect their income when they are qualified and have to pay any loans back.

It’s obviously also important to openly discuss how much, if any financial help you will be providing to them, and not leave them guessing. After all, this may have a significant impact on whether they end up applying for the genuine first choice or not.

Lastly, it’s crucial that you also go over the options for scholarships with your child as well, and make sure that they understand these entirely before they make their applications. After all, the can be complicated and confusing and they may even need to start working on things like their grades or other requirements before it gets to application time. Something that you can support them with and that can ultimately help them get into their first choice college.

I’ve said over and over again to parents, “You’ve got to look at the statistics when it comes to paying for college.” Before the list begins, before the college visits start and before the applications are completed, you MUST know how much it costs and if you can afford to pay for it. You should “follow the money” when choosing a college!

Where can you find the statistics? You can do your own research on College Navigator or CollegeData, or you look at these compiled from a survey by the Princeton Review.

“Best Financial Aid” #1 Bowdoin College (ME) / #25 Macalester College (MN)

“Best Career Placement” – #1 Harvey Mudd College (CA) / #25 Cornell University (NY)

“Best Alumni Network” – #1 Pennsylvania State University / #25 Union College (NY)

“Best Schools for Internships” – #1 Northeastern University (MA) / #25 Gettysburg College (PA)

“Best Schools for Making an Impact” – #1 Wesleyan University (CT) / #25 Kalamazoo College (MI)

“Top Colleges That Pay You Back for Students with No Demonstrated Need” – #1 Harvey Mudd College (CA) / #25 University of Michigan—Ann Arbor

These are more than statistics. They help you decide if your college investment will be worth the cost. Your student may not be thinking along these lines, but it’s your job to bring them down to earth.

Among the 200 colleges (135 private and 65 public) in the book:

the average grant to students with need is $26,800

the median starting salary of graduates is $55,700 and mid-career salary is $108,700.

Among the book’s 65 public colleges:

the average net cost of attendance (sticker price minus average grant) for in-state students receiving need-based aid is $12,700

the average admission rate is 53% and 12 colleges admit over 70%

Among the survey findings, 99% of respondents viewed college as “worth it,” but 98% said “financial aid would be necessary” to pay for it (65% of that cohort deemed aid “extremely necessary”).

Why should you consider these factors?

Before my daughter chose a college, we didn’t examine any of these factors. We compared financial aid packages, but we didn’t look for a college that was a good return on our investment. When it comes down to it, you spend a good amount of money on a college education. It’s an investment in your student’s future. We would never knowingly throw money into a bad investment or purchase a home high above market value, but every day parents invest their money in a college that won’t pay their student back.

Whether it’s career placement, networking, internships or tremendous financial aid, you should consider some of these colleges when making that final college list.

It’s financial aid award season. Students and parents have either received or will soon receive the award from the colleges that offered admission. How will this aid factor in to your student’s final decision?

But lurking between the lines in these award letters are some practices colleges use when offering admission and financial aid. Colleges will either lure students to accept their offer of admission, or discourage those students who were only offered admission to fill their quotas and inflate their numbers.

Front Loading

Front loading happens when colleges make their most generous financial aid award offers to applicants as a lure to attend. When students return the following year they may find their school has dropped their previously awarded grants and scholarships. Thousands of dollars may have been lost to the common practice of front loading, so ask these 5 questions:

Is the grant/scholarship renewable and if so for how many years? What you want is the money to continue until the student graduates. Bear in mind it is taking longer, four to six years, for those who graduate to do so. Find out the maximum number of times the award will be made.

What are the strings attached to keeping the grant/scholarship? It’s important to understand the terms of receiving free money awards before acceptance to make sure the student can and will perform them. He may have to keep his grades up, play an instrument, or be a member on a team. Find out the eligibility requirements each year including any additional paperwork necessary to keep them.

If the grant/scholarship is lost, what will replace it? Often student loans are the college’s substitution plan. However, there may be other grants/scholarships available. Ask about them and the application process. Be prepared to continue searching for these and have a college finance Plan B.

Will the college bill increase in following years and if so, by how much? Those renewable grants/scholarships may no longer cover the same portion of college costs if tuition rises. See what if any cost components like tuition/fees and room/board are capped or held at the freshmen level.

Will the grant/scholarship be increased to keep pace with any raised college costs? Be aware most colleges will not match tuition increases or increase free money aid when tuition rates increase. However, the college bill must continue to be paid.

Gapping

In admissions, college gapping is a term used in reference to colleges and financial aid awards. The gap between what you can afford to pay (your EFC) and what colleges offer in aid creates this gap. Gapping happens when a college makes an offer of admission and doesn’t back it up with financial aid. Quite simply, the college doesn’t offer enough aid to cover the difference between the cost of the college attendance and your expected family contribution.

Gapping is a serious business. Colleges use the tactic to “weed out” the good applicants from the average applicants. Quite simply, if your student is at the top of their applicant pool, they will receive the aid required to attend. If not, your student will be gapped, in the hopes they will reject the offer of admission.

It’s a numbers game. Colleges offer admission to more students than they can possibly accommodate. Gapping helps them lessen the number of students who accept those offers of admission.

Padding the Award

Colleges will pad the EFC numbers with federal student loans, federal parent loans and work-study. These should NOT be considered when determining if the college is gapping your student. All students qualify for federal student loans. College aid should only be in the form of merit scholarships and grants. If the difference between what you can afford and what the college offers is padded with loans, the college is gapping your student.

The lesson for parents and their college-bound students is to carefully scrutinize, analyze and question each item in their financial aid awards before bothering to compare one college’s offer to another. It may turn out that freshman year is a best deal at one place but if the total years until graduation are tallied, another choice may be the better bargain.

If the college is gapping your student it’s you and your student’s decision on whether or not to accept the offer of admission. If you want my advice–move on to the 2nd, 3rd or even 4th choice college with the good financial aid package. You will not only save a bundle, but your student will most likely be happier at a college that values his or her contribution.

Everyone wants a free ride for college. Unfortunately, it’s not that easy. Even athletic scholarships rarely provide students with a full ride for athletes.

Scholarships that pay all college expenses are available, however, if you know where to look. Here are four ways your student can win enough scholarship money to pay for all their college expenses.

Colleges with merit-aid

Good grades, good test scores, a stellar volunteer record and essay, can mean thousands of dollars in merit aid from the college. If your student is applying to one of the colleges on this list, he or she could score enough money to pay for all their college expenses.

Colleges with great scholarships for National Merit finalists

The PSAT is one way to win a full-ride scholarships. If your student is a National Merit finalist (which isn’t that difficult with a little preparation), he or she would be offered a full-ride scholarship and more. Here’s a list of colleges that offer scholarships to National Merit finalists.

Full-ride scholarships are offered to the students who are at the top of the applicant pool. The bar is set pretty high, but if your student is one of them, they could score a scholarship that pays all their college expenses. How does your student get to the top of the applicant pool? Apply to colleges where their SAT scores and GPA are higher than other students. This list will help you find those schools.

If your student works hard at applying for scholarships, it’s entirely possible to win enough scholarship money to pay for all their college expenses. Monica Matthew’s son, with her help, won $100,000 in scholarships. If you want to know how she did it, read her story and while you are there, purchase her simple how-to guide.

Finding and winning full-ride scholarships can be done. But it takes some effort: searching for the right colleges, doing the work in school, and applying for scholarships.

While many students are busy packing their bags and getting ready to leave for their first year at college, still others are working on their applications for the next round of admissions. Of course, if your child fits the latter category, it’s likely that they already have a college in mind that they wish to attend. Happily, by reading the post below you can find out about the tactics that will help them get into their first choice. Keep reading to discover more.

While many students are busy packing their bags and getting ready to leave for their first year at college, still others are working on their applications for the next round of admissions. Of course, if your child fits the latter category, it’s likely that they already have a college in mind that they wish to attend. Happily, by reading the post below you can find out about the tactics that will help them get into their first choice. Keep reading to discover more.