Debt from college tuition has skyrocketed over the last several years. Parents and students are weighing their ROI (return on investment) before making their college choices. As college costs have shot up, so has student debt. How can you pay for college without incurring debt?

According to the latest Quarterly Report on Household Debt and Credit, outstanding student loan debt stood at $1.58 trillion in the fourth quarter of 2021, an $8 billion decline from the third quarter. About 5 percent of aggregate student debt was 90+ days delinquent or in default in the fourth quarter; the lower level of student debt delinquency reflects a Department of Education decision to report current status on loans eligible for CARES Act forbearances.

That’s the bad news. But if you’re a savvy consumer and research the costs before signing on the dotted line, you should be able to go to college without incurring debt. Zac Bissonnette, author of DebtFree U, is proof that it can be done. He graduated from college with zero debt.

Believe it or not, you may be able to graduate without debt if you use these 10 ways to pay for college:

Looking for scholarships? There’s the usual scholarship search sites and scholarship books. You can find them at your student’s counselor’s office and locally. But what about social media–specifically Instagram? It’s a great place to find out about current and future scholarship opportunities.

Sometimes there are scholarships posted on these accounts that you might not easily find in a typical search. They post lesser known scholarships, often with fewer applicants. This increases your student’s chances of winning!

Not all colleges are created equal. But are you looking for the college bargains?

Community college. State University. Private liberal arts college. Trade or technical college. Top-tiered business college. Ivy League college. Not all colleges are created equal.

If that’s the case, what makes a good college? Some might think it’s a #1 rated NCAA football team, or a college with an Ivy League designation, or even a school that is highly selective. A good college (as in good fit) meets the following three criteria: academic, social, and financial. The college that meets or excels in all three should be the college your student chooses. Even the best college (based on reputation) isn’t a good college if the student neglects the opportunities he is given while attending.

In terms of financial fit, does the college fit into your family’s college budget?

Studies have shown that students who spent time working during college actually do better in the classroom. Students who work must learn how to structure and manage their time to work around class assignments. This translates into not delaying assignments and scheduling time to study for exams. However, many experts suggest that freshmen students wait until the second semester to take on the added responsibility of a job. This allows them time to ascertain their academic strengths and decide whether or not a job would detract from their study time.

When college students do decide to work, there are three options available to them: on-campus jobs, off-campus jobs and internships. Each of these job opportunities has its own set of advantages.

Many students neglect applying for scholarships with small awards. However, every small award your student receives means more free money to pay for college.

The RevenueZen Social Selling Scholarship is an award for any current or soon-to-be undergrad who is looking to innovate the hiring process. In an ideal world, what would hiring and applying for a job look like? How will you stand out? The RevenueZen Scholarship has a brief submission process, and applicants will be judged on their ability to convey their idea for an innovative social selling process focused on getting hired at a specific company.

Financial aid can be a confusing part of the college application process. Even if you can afford to pay for college, it’s a good idea to learn what aid is available and apply for it. You aren’t obligated to accept it, but most students qualify for some form of aid and, if it’s available, why not use it?

What is financial aid?

Financial aid is intended to make up the difference between what your family can afford to pay and what college actually costs. With college tuition rising rapidly, more than half of the students currently enrolled in college receive some sort of financial aid to help pay for college. The system is based on the premise that anyone should be able to attend college, regardless of financial circumstances. However, students and their families are expected to contribute to the extent that they are able.

There are two types of aid: need-based, and non need-based. Need-based aid includes grants and scholarships that are issued based on the family’s ability to contribute to education costs. Non-need-based aid is allocated solely based on availability, not need.

There are three main types of financial aid: grants and scholarships, loans and work study.

What is “free” money?

Not all aid is equal and the best aid is the aid you don’t have to pay back. It’s like getting a huge coupon of savings to use for your college education.

What types of education loans are available?

Not all college loans are equal.

There are two types of government-based loans: subsidized and unsubsidized. Subsidized loans have lower interest rates and are awarded based on the student’s financial need with interest deferred until after graduation. Unsubsidized loans are awarded without regard to financial need with interest payments beginning immediately and regular payments due after graduation.

What is work study?

The Federal Work-Study Program provides a method for college students to earn funds to be used toward their education. The program is based on financial need and students must be accepted into the program to qualify which is determined by completing the Free Application for Federal Student Aid or FAFSA.

What is the FAFSA and do I need to file it?

The FAFSA is the Free Application for Federal Student Aid and you should apply if you want any chance to receive federal and state student grants, work study, loans or merit-based aid. If you don’t complete the FAFSA, you can’t apply for student loans. Colleges also use these figures when determining financial aid eligibility for grants and scholarships. Plus, many states use your FAFSA data to determine your eligibility for their aid.

The FAFSA is available on Oct. 1 of every year and you should complete it as close to that date as possible in the fall of your senior year. Aid is dispersed on a first-come, first-served basis. The sooner you apply, the more likely you will receive a portion of the financial aid pie.

What is the EFC?

The Expected Family Contribution (EFC) is how much money your family is expected to contribute to your college education for one year. Typically, the lower your EFC, the more financial aid you will receive. Factors such as family size, number of family members in college, family savings, and current earnings (information you provide on the FAFSA) are used to calculate this figure. Once your FAFSA is processed, you will receive a Student Aid Report (SAR) with your official EFC figure.

You can calculate your EFC by visiting FinAid.org.

What is an award letter and how do you use it?

As the offers of admission arrive from colleges, the financial aid award letters will follow. They can be confusing and vague. Added to the confusion is that every award letter is different, making it hard to easily compare them side by side.

Thankfully, there are tools available and information to help you look at these letters for what they are: the college’s pitch for you to accept their offer of admission. You are in control of this process and you hold the cards. It’s your decision to accept or reject their offer based on the amount of aid they are willing to give you. Money, in this situation, is everything.

If a college wants you to attend, they will back it up with money. No money means their offer is probably based on filling a quota and expecting you will decline to attend. And you should. Who wants to attend a college that doesn’t value you as a student?

Summer jobs are great for teenagers who want to save money for college. That money is great for textbooks, entertainment and other expenses. But what if your student could earn scholarship dollars while working at a part-time job during high school?

They can! Many companies award scholarships to their student employees. If your student wants to work during high school, why not cash in on some of this FREE money?

Here are just a few companies awarding scholarships and educational funds to deserving student employees:

To kick off the 2019 scholarship announcements, Chick-fil-A surprised 12 Team Members on stage at the company’s annual conference Tuesday with the news that they were this year’s $25,000 True Inspiration Scholarship recipients. The celebration will continue throughout March as local Chick-fil-A franchise Operators present $2,500 Leadership Scholarships to 6,016 Team Members across 47 states.

Starbucks is committed to the success of our partners (employees). Every benefits-eligible U.S. partner working part- or full-time receives 100% tuition coverage for a first-time bachelor’s degree through Arizona State University’s online program. Choose from over 80 diverse undergraduate degree programs, and have our support every step of the way.

Employees and their families can qualify for one of the following scholarships:

Up to 3 James W. McLamore WHOPPER® scholarships of $50,000 granted to the most highly qualified students demonstrating leadership, substantial work experience and financial need

Up to 12 Regional awards of $5,000 granted to the two most qualified employees in each of six regions from the pool of eligible and complete applicants

One (1) Steven M. Lewis Foundation award of $5,000 granted to the most qualified U.S. Restaurants employee from the pool of eligible and submitted applicants aligned to U.S. Restaurants

Up to four (4) Bravokilo, Inc./Bravotampa, LLC awards of $5,000 granted to the most qualified Bravokilo, Inc./Bravotampa, LLC employees from the pool of eligible and submitted applicants aligned to Bravokilo, Inc. or Bravotampa, LLC

One (1) Ghai Management award of $5,000 granted to the most qualified Ghai Management employee from the pool of eligible and submitted applicants aligned to Ghai Management

One (1) Carrols LLC award of $5,000 granted to the most qualified Carrols LLC employee from the pool of eligible and submitted applicants aligned to Carrols LLC

Additional award designations as determined by Burger King Corporation, participating franchisees of the BURGER KING® system or BURGER KING℠ McLamore Foundation

The Publix tuition reimbursement program can help cover the cost of college classes. This program is available to part-time and full-time associates who are seeking graduate or undergraduate degrees. In addition, some individual courses, online programs, and technical training in appropriate areas of study can also be covered. As long as an associate has six months of continuous service and works an average of 10 hours per week (which leaves plenty of time for studies!), they can be covered in this program.

For a list of 36 companies who offer either scholarships or tuition reimbursement, EStudentLoan has compiled a list–click here.

The Krazy Coupon Lady has also compiled a list of companies that offer money for college is you’re an employee–click here.

October 1 is on the horizon and that means the FAFSA will be available for students to complete and file. Believe it or not, many students don’t bother completing it and that’s a decision you and your student might regret.

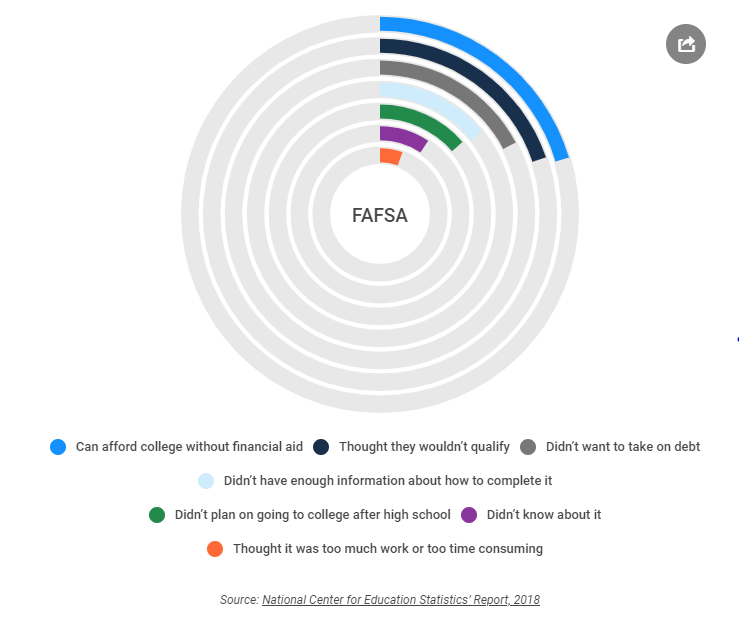

According to the National Center for Education Statistics, Only 65% of high school seniors complete the FAFSA, Why don’t more fill it out? Most either can afford college without financial aid or think they won’t qualify for financial aid. Other reasons include a lack of information — and just planning on skipping college entirely.

Completing the FAFSA is an essential step of the college application.

Why bother completing the FAFSA if you don’t need financial aid?

Even if you and your student can afford to pay for college, why would you pass up free money? Colleges use the FAFSA when distributing merit aid and even some private scholarships require a completed FAFSA.

If you need financial aid, how can completing the FAFSA help?

If you need some form of financial aid to pay for a college education, you MUST complete the FAFSA. In order for students to qualify for federal student loans, state loans, and work-study, they must submit the form. The FAFSA is also required if you plan to take out a Parent PLUS loan to help your student pay for college.

In addition, many students are eligible for federal Pell Grants. High school graduates who didn’t complete a federal financial aid application missed their opportunity for part of $2.6 billion in free money for college, according to NerdWallet’s annual analysis of federal financial aid data.

The money went unclaimed by 661,000 members of the Class of 2018 who were eligible for a federal Pell Grant but didn’t complete the Free Application for Federal Student Aid, or FAFSA.

How much time does it take to complete the FAFSA?

The FAFSA has over 100 questions, which can take anywhere from a half hour to an hour to complete. According to data compiled by Finder.com, new applications less than an hour, averaging 35 minutes. Renewing your application takes even less time — 23 minutes on average. Filling out the FAFSA for the first time takes the longest since you need to fill in answers for each required question.

The bottom line: complete the FAFSA. It doesn’t take that long and most students qualify for some form of financial aid. That doesn’t mean you have to accept it, but why not have that option? And you certainly don’t want to miss out on some of that FREE money!

I

received an email from a concerned parent whose student was going to be

attending orientation next week. In the email, he confessed that he might need

some help with information regarding financing his son’s college education. I was

surprised that he waited so long. Unfortunately, I had to advise him that at

this point his only options were private loans and advise his student to apply

for scholarships over the summer.

Parents should consider college funding even before their student applies to college. The inevitable result of lack of planning is parents and students borrowing to pay and usually borrowing more than they can repay after graduation.

What

do the statistics say?

With

school starting shortly, student loan borrowing often appears in the news. It’s

especially prevalent now with presidential candidates promising to erase

student loan debt. Wherever you stand in the political landscape, it’s clear

from the statistics that students have borrowed more than they can repay.

According

to a 2018 report by the Federal Reserve Bank of New York, as many as 44.7

million Americans have student loan debt, that’s one in five adult

Americans. The total amount of student loan debt is $1.47 trillion as

of the end of 2018 — more than credit cards or auto loans.

How

do you make wise financial choices?

Before applying to college, you and your student should investigate the cost. You can gather the information either on the college website or by using College Navigator. When viewing these figures, you should also research the college’s financial aid statistics—what percentage of students are awarded aid, how much aid is awarded and how much do students typically borrow. Since every family’s financial situation is different, these figures should help determine if the college is affordable to attend.

How

does financial aid play into the equation?

If

you complete the FAFSA, your student will receive some form of financial aid.

The most common is student loans, but colleges also award grants and merit aid

as well. Always complete the FAFSA, even if you don’t think you will qualify

for aid. Colleges use the information on the FAFSA when awarding scholarships

and grants. No FAFSA, no aid.

What’s the key to avoid borrowing too much?

Use repayment calculators before you sign on the dotted line. The rule of thumb is that students should only borrow as much to pay for college as their first year’s salary. By keeping your debt under one year’s salary, you won’t have to put more than about 10% of your income towards student loan payments. Borrowing more than your student can afford to repay sets them up for overwhelming debt after graduation. Your student can look at salary comparisons for their anticipated career at PayScale.com.

How

can you avoid borrowing to pay for college?

The key to not borrowing to pay for college is to receive merit aid, grants, and outside scholarships. Your student should apply to a college at the top of his or her applicant pool. This means the college will be more likely to award aid to attract your student. Grades and standardized test scores are also a key factor in awarding aid. Your student should focus throughout college to pursue excellence in these areas. And, don’t forget outside scholarships. Your student should focus time and effort in applying to every scholarship he or she qualifies for. This means starting early and planning to submit the best application. Click here for scholarship application tips and see how your student can win enough money to pay for college.

Finally, borrow wisely. Only borrow what you need. Your student can borrow the maximum amount, but only borrow what is necessary. Just because you can, doesn’t mean you should. Choose the loans with the lowest interest rates first.

If you’re a parent with a college-bound teen you might be feeling just a bit overwhelmed. With tuition costs rising and many colleges reducing their financial aid packages, it’s easy to wonder if you’ll be able to afford that hefty college price tag and focus on college sticker shock. Whether you are looking at fall college admission payments coming due, or you have several years to go before forking over the cash, you’ll appreciate these simple cost savings tips.

Encourage your teen to search and apply for scholarships. There are all types of scholarships available for all types of students at all ages and education levels. Summer is the perfect time to search and apply, thus conquering summer boredom.

Get college credit early with AP exams. If your teen is enrolled in high school AP courses, make sure they take the AP exams. If they score well, they will receive college credit, which can save you thousands of dollars in tuition alone.

Don’t discount private universities. Your EFC (Expected Family Contribution) will be the same no matter which college your teen attends. Private universities often have substantial alumni donors and also have the largest aid packages with many paying the total cost of tuition.

Consider programs

that provide funds during college in exchange for a service commitment. These

programs such as ROTC, AmeriCorps, VISTA and

the Peace Corps offer tuition reimbursement, stipends and also provide an

opportunity to serve.

Apply for financial

aid even if you don’t think you will qualify. Every family should

complete the FAFSA (Free Application for Federal Student Aid). Every college

uses this form to distribute need-based and non-need based aid. Even if you

don’t qualify for need-based aid, your teen might qualify for an academic

campus-based scholarship.

Be a penny pincher. You

can save big bucks on textbooks, computers, meal plans, dorm furnishings and

transportation. Investigate alternatives to paying top dollar for new items and

save on second-hand items.

Encourage your teen

to take summer classes at your local community college. The

cost for these courses will be substantially less that at a four-year

university. However, make sure that these credits will transfer to your teen’s

chosen college upon completion.

Before your teen heads off to college, create a simple budget that will

help your teen and your family plan for college-related expenditures. These

simple college cost savings tips should help you save a large chunk of change;

and in today’s economy, every dollar counts.