When my daughter opened the email, I saw the joy light up her face. Congratulations! She got in. She did it. Her dream college, the one she had been talking about for years, was offering her a spot.

For a moment, everything felt perfect.

I let myself soak in her excitement. I hugged her tightly. I even let myself imagine what it would be like—move-in day, walking around that beautiful campus, wearing the school sweatshirt with pride. I thought about all the years of hard work, the late-night study sessions, the endless applications, the moments of doubt she had overcome. This was supposed to be it.

For many students across the country, taking out a student loan is the only way they can afford to get the education they want and need.

While other options, like scholarships or financial aid, are available for students meeting the criteria for others whose parents can help them or can’t cover the entire four-year tuition, student loans can bridge the gap and are a necessary evil.

However, not all student loans are the same. Understanding the financial agreement you’re signing up for and knowing how to find the best student loans can empower you, giving you the control to avoid some of the common pitfalls of student loans and make more informed decisions. So here goes.

Paying for college today can be stressful. Reading all the posts from parents on Facebook underscores the fact that college is expensive and parents are trying to pay for it without borrowing or graduating with massive student loan debt.

Today’s guest post is by Bob Collins, VP of Financial Aid at Western Governors University.

WGU students graduate with half the debt of their peers nationwide

Education is linked to the eradication of poverty and the promotion of prosperity, but evidence that college students graduate with excessive debt continues to pile up year after year. With student interest rates at their highest in the last decade, our current economy serves as a reminder that students should make informed decisions to borrow wisely.

Western Governors University (WGU) was established in 1997 with a mission to expand access to high-quality, online and affordable higher education. WGU serves more than 150,000 students nationwide and has more than 340,000 graduates in all 50 states.

I have had some serious conversations recently with a parent and student who applied to college, was accepted, and was shocked at the cost. The parent didn’t want to disappoint her daughter. The daughter wanted desperately to go to an out of state college that would cost over $50,000 per year with no financial aid.

After speaking with the daughter at length, she decided to defer for a year, work, save her money and apply for scholarships. Taking out loan was not appealing to either of them and I completely agreed.

Parents and students should consider college funding even before their student applies to college. The inevitable result is the parents and students borrowing to pay and usually borrowing more than they can repay after graduation.

With a new school year quickly approaching,

many parents are figuring out how their child is going to afford college.

According to CollegeBoard, the average student budget for the 2019-20 academic

year was $26,590 for students attending a four-year university. This figure

includes the cost of living on campus, which may be required of incoming freshman students.

This means your child’s education could cost

well over six figures. And no parent wants their child to start their adult

life with that amount of debt.

As a parent, you can help guide your child to make smart decisions

that will impact their finances for years to come. This begins with choosing an

affordable school.

There are also other ways to help pay for the

cost of attendance and living expenses. Here’s how to help fund college costs

and ways to borrow wisely.

Apply for financial aid

opportunities before borrowing

Before you or your child

take on debt to pay for college, you should exhaust all other available

resources.

Your child can access financial aid opportunities, like grants, scholarships and work-study programs, by

completing the Free Application for Federal Student Aid (FAFSA).

The FAFSA filing window

is October 1 to June 30 for each upcoming academic year. Keep in mind that some

financial aid is available on a first-come, first-serve basis, and cutoff

deadlines vary by state. Encourage your child to complete their application as

early as possible.

Also explore third-party

scholarship opportunities through your employer, local community organizations and

online databases. Each additional scholarship or grant — even if it is only for

a few hundred dollars — can prevent your child from taking on more student loan

debt.

How to borrow wisely for college

Once your family has explored all financial

aid opportunities and pooled existing resources (e.g. 529 college savings plan

and other family contributions), your child may still need to turn to student

loans.

Whether your child is taking out loans in

their own name or you’re borrowing on their behalf, it’s important that your

family only borrow what is needed to fill the remaining financial gap.

The first way to approach student loans is

through federal loans. Federal loans have more flexibility and have certain

protections and benefits. This is why it’s best to maximize federal loan

opportunities before taking out private loans.

For example, your child can enroll in a

repayment plan that matches their financial situation and may be eligible for

loan forgiveness opportunities.

Your child should borrow funds in this order:

Direct Subsidized Loans.

Subsidized loans typically have the lowest rates, and the government will

cover any interest that accrues while your child is in school.

Direct Unsubsidized Loans.

Unsubsidized loans aren’t need-based, so any student can qualify for them.

However, your child is responsible for the interest that accrues during

school.

Private loans. Your child

will likely need a cosigner to qualify for a private loan. Shop around

with various private lenders to find the lowest rate and best terms for

your credit.

You may also have the option to take out a

federal Parent PLUS loan in your name to help fund your child’s

education.You’ll be solely financially responsible for the loan — not your

child.

Make a debt repayment plan

Student loan borrowers

should always be aware of interest charges that will accrue during school and

after graduation. These charges should be included in their overall financial

plan.

Your child should also start making a debt

repayment plan as soon as possible. Popular student loan repayment methods

include enrolling in an income-driven repayment (IDR) plan or refinancing student loans after graduation to

get a lower interest rate.

When considering refinancing federal loans

into private student loans, it’s important to understand the consequences of

losing out on federal benefits and protections, like loan forgiveness and

forbearance.

The earlier your child plans for their educational costs, the more likely they can save money during their college experience and beyond.

Our guest post today is by Travis Hornsby, CFA, and Founder and CEO of Student Loan Planner. He lives with his wife in St. Louis, MO, where he loves thinking up new student loan repayment strategies and frequenting the best free zoo in America. As one of the nation’s leading student loan experts, he has consulted on $500 million of student debt personally.

It’s been in the news—Bernie Sanders has introduced a bill

to cancel student loan debt. I don’t want to share any political viewpoints

here. I want to express what this communicates to the past and future

generations of students.

To the past generation of students

I have two children who incurred student loan debt. One of them worked hard to pay hers off. The other is still paying his. My daughter got good grades in high school, earned scholarships and borrowed wisely. After high school, my son entered the military and after completing four years of service used the G.I Bill to pay for some of his education. For the rest, he did not borrow wisely. He chose to attend an expensive college that he could not afford, and he will be the first to tell you he made a mistake.

But he won’t say his debt should be cancelled. And my

daughter, who worked hard to pay hers off, will feel this is a slap in her

face. They both had choices and have lived with those choices. No one forced

either of them to go to a college that required them to take out student loans.

It was their choice and they take responsibility for it.

Students who have worked hard to pay off their debt or made a choice to attend a college they could afford are outraged by the thought that others will not have to pay back their debt. It’s unfair and communicates the wrong message. Why should those who worked hard to pay their debt off have to pay for those who will not?

To the future generation of students

College is expensive and the cost of an education is rising

every year. But teaching your children to make wise financial choices is a

crucial part of parenting. Not every student needs to go to an expensive

college. There are less expensive alternatives, colleges that allow students to

work while they attend, and scholarships available to help pay for college.

Forgiving all student loan debt teaches future students that

it’s not important to make wise financial choices. It teaches them that

everyone deserves a free ride and hard work is not rewarded. We are raising a generation

of new leaders that will soon forget that hard work and sacrifice reaps reward.

Why work hard if you can get it for free? Why pay off the debt you incurred due

to unwise financial choices if the government is going to step up and forgive

it?

My opinion

If I’m honest, I would love for my son’s student loans to be forgiven. But I know, as a parent, that is not the best for him, and he would agree; he borrowed the money and he should have to repay it. We must teach future generations there are consequences to actions and this includes incurring debt that you cannot repay. It simply comes down to the fact that we all have a free will and can choose to spend more than we can repay or save and borrow wisely. It’s something my parents taught me and because of wise financial choices, they paid for what they could afford and saved for what they could not.

At some point, everyone is responsible for their own choices. Those students who worked hard and paid for college without incurring debt should be rewarded. Those who incurred debt, should be held accountable and required to repay it. It’s a tough pill to swallow but a lesson we all need to learn in life.

Many families are unrealistic about covering the cost of an expensive college education. Many students admitted that paying for the education at a more expensive university would put a financial burden on their families, but they were still willing to risk it based on their perceived value of that education.

“When three generations of a family collaborate to tackle college costs and fail, the results can be catastrophic. Credit profiles are destroyed, homes and retirements are put at risk, and families land in bankruptcy court. Even then, in most cases higher-education loans, which average more than $30,000 per bachelor’s degree recipient, can only be deferred in bankruptcy, not discharged.

What you’re seeing now in the student-loan area is not only the debtor, but the family of the debtor,” said Manhattan bankruptcy lawyer Dave Shaev. “Mom and Dad are usually the co-signers, and sometimes Grandma or Grandpa are having to dive into retirement funds and home equities to try to bail out a daughter or son with student loans, because the jobs they are getting do not allow them to keep up on the payments.”

Being realistic about student debt and earning potential after graduation is an important part of your college decision. Here are some tips to help make that decision:

Research the jobs that

involve your intended major. Don’t limit

yourself to the obvious. You might find a career path that you had not even

considered.

2. Investigate the

earning potential of the career

These figures can be

easily obtained through the Bureau of Labor Statistics projected earnings

charts. Be realistic. You won’t be paid at the top of the scale right after

graduation. Use the lowest percentage for your figures as a conservative

estimate.

3. Learn about loan repayment

If you are borrowing

money to attend college, don’t just assume you will make enough money to pay

back those loans. Research repayment amounts (and monthly payments) to

determine how much of your salary will go towards student

loans.

4. Consider that life is more than dollar signs

If you are making five figures and employed at a job you detest, the money won’t soothe your misery. Being financially secure is everyone’s goal, but sometimes working at a job you love is worth its weight in gold. A career as a teacher can be as rewarding as being a doctor. You know yourself better than anyone else—pursue your passion.

5. The highest priced

education is not always the best

A high-priced higher

education is not always worth the dividend it pays. Investigate the cost of

tuition and weigh that against your future earning potential. It is wise to

consider community college, investigate trade schools, evaluate state college

cost versus that of private universities, and even consider online accredited

learning.

That degree from a

so-called prestigious university might look

great on your wall; but is it worth cost? Be a wise consumer and don’t go into

debt on the promise of a five-figure salary. Study the statistics, put some

thought into the process, and make an informed decision.

The thought that crosses every students mind is the dreaded debt they will inevitably find themselves in years and years down the line. It seems that students are now facing an uphill battle when it comes to their student loan debt. You will struggle to get a credible job without the relevant qualifications, which means at some point you’re going to need to go and study at college. Unfortunately, college fees do not come cheap. Many people have to boycott college altogether because they simply can’t afford it. It’s such a shame that many youngsters have to miss out on getting the best education because money is short. If you are lucky enough to get into your chosen subject of education, here are a few pointers which will help you to avoid the dreaded debt.

Social Butterfly Without the Burden

You’ve gotten into the college of your dreams and you can’t wait to make new friends and memories, but you’re a little worried about your budget. You are not alone. Every single person is worried. Socializing at college doesn’t have to be super expensive. There are several ways in which you can save money and still have a great time. Join loyalty schemes and get to know which bars and restaurant your campus is associated with. The chances are you will be able to get discounts all year round, which means cheap drinks and food whenever you and your friends go out. Change up how you socialize with your friends too. Spend more time around people’s places instead of going out and hold movie nights instead of taking a trip out to see the latest blockbuster.

Room and Board Can Cost A Little

Room and board costs can stump a lot of students. Seriously, how can it cost so much to live in a pitiful little room with no bathroom? If you haven’t already thought about it, maybe you could consider online education to save yourself a lot of money. Partaking in an online bsw, for example, would allow you to stay at home and would cut your student debt almost completely. By opting to be educated virtually you wouldn’t be overburdened with outrageous costs, but keep in mind you need to be super motivated in order to get a degree from an online format.

Save, Save, Save

Before your further education suddenly hits you like a brick wall you should consider saving up some cash so you have got a head start. The summer before you’re due to head off to college you should definitely consider getting a job. It will not only give you a boost to buy all of the things you’ll need when you’re first moving away, but it will also motivate you to earn some money whilst you’re getting your education. Many students find it useful to take on a part-time job whilst they’re studying. It will ease the burden much more in the future.

So take these points into consideration if you’re due to start your higher education. Maybe you have a younger sibling who is ready to go to college and you want them to learn from your mistakes. Let’s start imparting our wisdom on others and stop the vicious cycle of student debt!

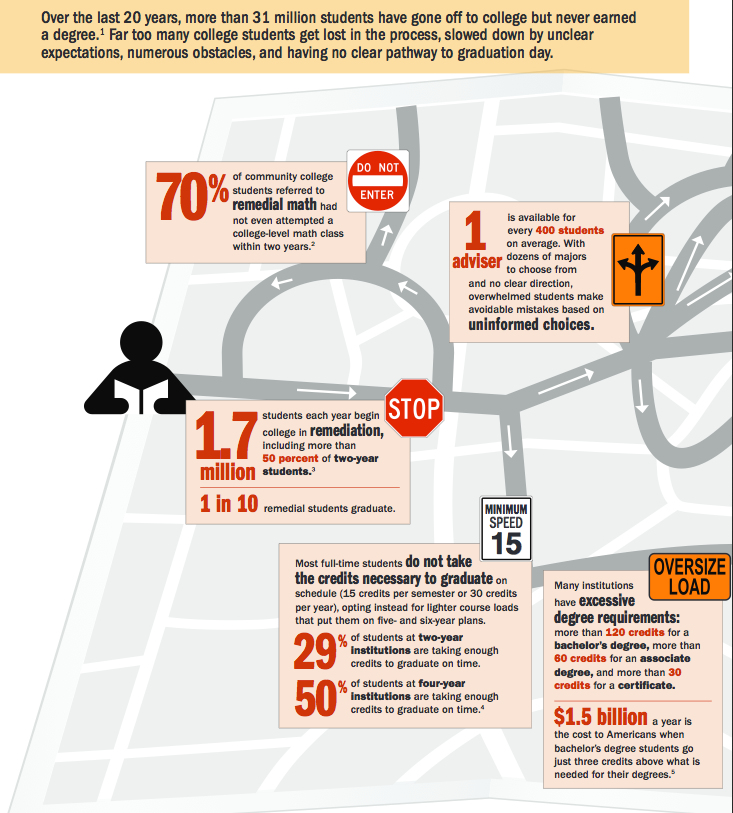

Did you know that at most public universities, only 19 percent of full-time students earn a bachelor’s degree in four years? Even at state flagship universities — selective, research-intensive institutions — only 36 percent of full-time students complete their bachelor’s degree on time.

Nationwide, only 50 of more than 580 public four-year institutions graduate a majority of their full-time students on time. Some of the causes of slow student progress are inability to register for required courses, credits lost in transfer and remediation sequences that do not work. Studying abroad can also contribute to added time and credits lost when abroad. According to a recent report from CompleteCollege.org some students take too few credits per semester to finish on time. The problem is even worse at community colleges, where 5 percent of full-time students earned an associate degree within two years, and 15.9 percent earned a one- to two-year certificate on time.

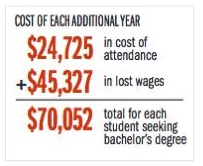

What is lost when a student doesn’t graduate in 4 years?

MONEY! My good friend, and college counselor, Paul Hemphill of Planning for College put it into perspective recently. (See chart to the right). It’s not just the cost of the education that your student loses, but the earning potential over the additional year or years. Nothing speaks louder than cold, hard numbers.

What can parents do to ensure on-time graduation?

It’s not a difficult task, although the numbers might speak otherwise. Taking control of the process and making a plan will go a long way in ensuring on-time graduation

Show your student the numbers—Nothing speaks louder than showing your student a loss of thousands of dollars in earning potential if they don’t graduate on time.

Help them plan their major and degree plan, ensuring it can be done in 4 years—Help them plan, ask questions of their advisors, and have solid discussions about their career and/or major.

Encourage AP testing and dual-credit courses—With AP testing and dual-credit courses, a student can enter college with multiple credits out of the way. The cost of these tests and courses pales in comparison to the cost of a college credit and extra money paid if they don’t graduate on time. It’s conceivable that with the right planning, a student can graduate in less than 4 years.

Attend community college for the basics during the summer before college—Not only will your student get some courses out of the way at a cheaper rate, they will enter college with credits under their belt.

Use some tough love—Explain the importance of graduating on time and explain that you will support them for 4 years only. After that, the cost is on them. Nothing motivates a teen more than realizing they will have to pay for college themselves.

Below is a neat little graphic (courtesy of Paul Hemphill) breaking it down for you.

What is lost when a student doesn’t graduate in 4 years?

What is lost when a student doesn’t graduate in 4 years?